Purchase the current version only, no updates will be sent.

$2,575.00

Purchase the current version only, no updates will be sent.

Our Assured Print Pricing program offers predictable monthly pricing and capped year-over-year price increases. Choose between 2, 3, 5, and 10-year agreements. All updates, new editions, and revisions are included in your monthly payment and delivered automatically, as soon as they become available.

$214.00/month

Learn more](https://store.legal.thomsonreuters.com/law-products/proviewLearnMore)

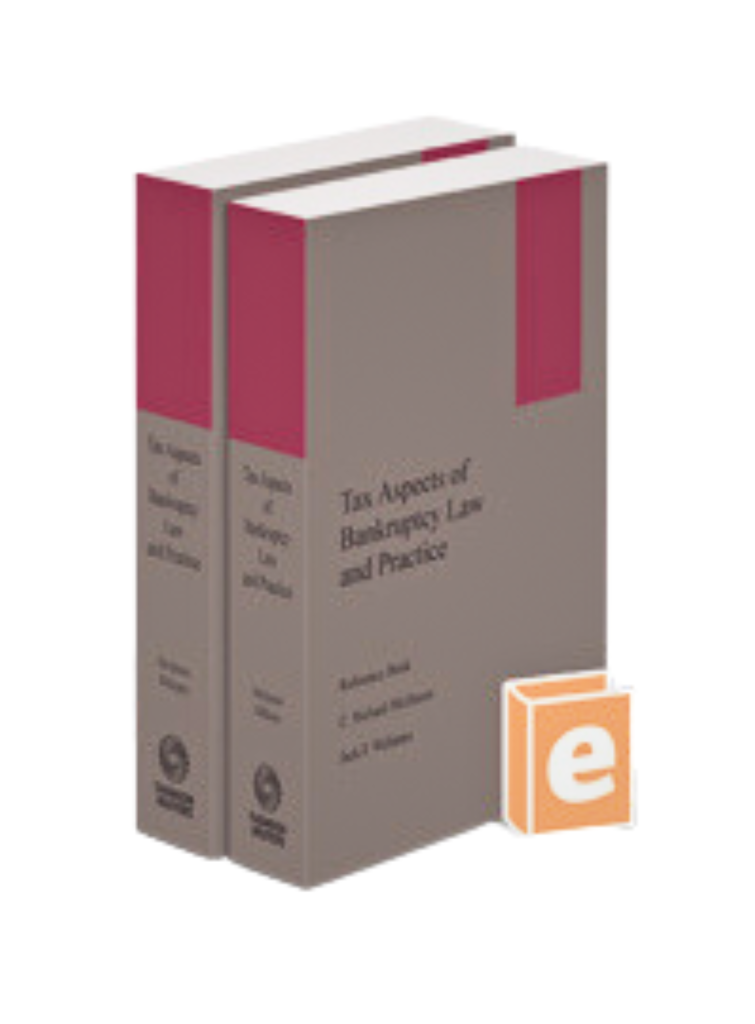

Tax Aspects of Bankruptcy Law and Practice includes detailed discussions of all the areas of tension between the Bankruptcy Code and the Internal Revenue Code including bankruptcy tax issues from each perspective. It offers the best way to anticipate and take advantage of the tax issues when filing and administering a bankruptcy case and provides analysis of relevant tax decisions handed down by the courts.

The text reviews the IRS’ position in unresolved areas and the options available to the debtor (including dischargeability of the debtor’s taxes), the debtor’s insiders, and other creditors. It discusses the application of the automatic stay to tax collection efforts, setoffs, and refunds. Other topics include:

It also includes the separate tax entity rules of IRC §1398 and federal tax liens both in and out of bankruptcy.

CHAPTER 1. OVERVIEW OF BANKRUPTCY LAW I. INTRODUCTION TO BANKRUPTCY LAW § 1:1 History of bankruptcy law § 1:2 Policies embodied in the Bankruptcy Code § 1:3 Individual debtors § 1:4 Business debtors II. TYPES OF BANKRUPTCIES § 1:5 Introduction § 1:6 Chapter 7 § 1:7 Chapter 9 § 1:8 Chapter 11 § 1:9 Chapter 12 § 1:10 Chapter 13 III. WHY BANKRUPTCY?—BANKRUPTCY AS A FINANCIAL TOOL § 1:11 Generally IV. JURISDICTION AND COMMENCEMENT OF A BANKRUPTCY CASE § 1:12 Generally § 1:13 Voluntary cases § 1:14 Involuntary cases § 1:15 Dismissal or conversion to other chapters V. WHO MAY BE A DEBTOR IN BANKRUPTCY? § 1:16 In general § 1:17 Under Chapter 7 § 1:18 Under Chapter 11 § 1:19 Under Chapter 13 § 1:20 Debtor’s duties VI. FUNDAMENTAL ISSUES IN BANKRUPTCY § 1:21 Major concepts in Bankruptcy Code § 1:22 Automatic stay § 1:23 —The scope of the automatic stay § 1:24 —Acts in violation of the automatic stay § 1:25 —Exceptions to the automatic stay § 1:26 —Relief from the automatic stay § 1:27 — —Filing requirements § 1:28 — —Seeking relief from the automatic stay § 1:29 —Termination of the automatic stay § 1:30 The bankruptcy estate § 1:31 —Property of the estate § 1:32 Exempt property in bankruptcy § 1:33 —Bankruptcy exemptions § 1:34 —Exemption procedures § 1:35 —Objections to declaration of exemptions § 1:36 —The exemption avoidance power § 1:37 The debtor’s right to redeem tangible personal property VII. THE CHAPTER 11 CASE § 1:38 In general § 1:39 Filing a plan of reorganization § 1:40 Contents of a plan and disclosure statement § 1:41 Classification of claims § 1:42 Funding alternatives for plans of reorganization § 1:43 —Sale of assets § 1:44 —Avoidance powers § 1:45 —Postpetition financing § 1:46 —Equity-for-debt swaps § 1:47 —Equity infusions § 1:48 Future operations § 1:49 Acceptance and confirmation of a reorganization plan § 1:50 Plan confirmation § 1:51 —Confirmation under § 1129(a) § 1:52 —Tax claims and issues § 1:53 —Cram down § 1:54 —Competing plans § 1:55 Effect of confirmation § 1:56 Modification of the plan § 1:57 Discharge under Chapter 11 VIII. THE CHAPTER 13 CASE § 1:58 In general § 1:59 Elements of the plan § 1:60 Role of the Chapter 13 trustee § 1:61 Plan confirmation § 1:62 —Effect of confirmation § 1:63 Modification of the plan § 1:64 Discharge under Chapter 13 IX. CASH COLLATERAL AND DEBTOR TRANSACTIONS § 1:65 Viability of business § 1:66 Cash collateral § 1:67 —Definition of cash collateral § 1:68 —The debtor’s use of cash collateral § 1:69 Transactions with the debtor X. EXECUTORY CONTRACTS AND UNEXPIRED LEASES § 1:70 What is an executory contract or unexpired lease? § 1:71 When must the trustee assume or reject? § 1:72 The standard for assumption § 1:73 The special cases of real property—Unexpired lease of nonresidential real property where the debtor is the lessee § 1:74 —Unexpired lease of real property where the debtor is the lessor XI. AVOIDANCE POWERS § 1:75 In general § 1:76 Trustee’s strong-arm powers under § 544(a) § 1:77 Trustee’s powers under § 544(b) § 1:78 Avoidable preferences under § 547(b) § 1:79 —Elements—A transfer of the debtor’s property § 1:80 — —To or for the benefit of a creditor § 1:81 — —For or on account of an antecedent debt § 1:82 — —Made within 90 days before bankruptcy, or, if the transferee is an insider, within one year of bankruptcy § 1:83 — —The debtor is insolvent § 1:84 — —Preferential effect § 1:85 —Defenses § 1:86 — —Contemporaneous exchange § 1:87 — —Payment made in the ordinary course of business § 1:88 — —Enabling loans § 1:89 — —Subsequent advancement of unsecured credit § 1:90 — —Floating liens § 1:91 — —Statutory liens § 1:92 — —Payment of debt for domestic support obligations § 1:93 — —Small consumer debt payments § 1:94 — —Small business debt payments § 1:95 — —2005 Act changes § 1:96 Statutory lien avoidance under § 545 § 1:97 Fraudulent transfers under § 548(a) § 1:98 —Constructively fraudulent transfers § 1:99 — —Lack of reasonably equivalent value § 1:100 — —Statutorily defined financial distress § 1:101 — —Insolvent or rendered insolvent § 1:102 — —Left with unreasonably small capital § 1:103 — —Left with an inability to pay debts as they become due § 1:104 Changes to fraudulent transfer law § 1:105 —Two-year reach back period § 1:106 —Insider employment contracts § 1:107 —Condemnation of certain asset-protection strategies § 1:108 Post petition transfers under § 549(b) § 1:109 Setoff under § 553 § 1:110 —Right to setoff § 1:111 —Limitations on a creditor’s right to setoff § 1:112 — —Calculation of possible recovery § 1:113 — —Additional analysis and illustrations § 1:114 Avoidance power liability under § 550 XII. CLAIMS AND DISTRIBUTION § 1:115 In general § 1:116 Chapter 7 case § 1:117 Chapter 11 case § 1:118 Chapter 13 case § 1:119 Claims and distribution § 1:120 Secured claims § 1:121 Unsecured claims § 1:122 Priorities under the Bankruptcy Code § 1:123 Distribution to creditors in a Chapter 11 case § 1:124 Distribution to creditors in a Chapter 13 case § 1:125 Subordination of claims § 1:126 Establishing and protecting claims XIII. THE DISCHARGE § 1:127 Discharge in general § 1:128 Prior denial of discharge § 1:129 Effect of discharge § 1:130 Nondiscrimination provision § 1:131 § 727 discharge § 1:132 § 1141 discharge § 1:133 Scope of discharge § 1:134 Chapter 7 discharge § 1:135 Chapter 13 discharge § 1:136 The discharge hearing § 1:137 Reaffirmation § 1:138 Redemption § 1:139 Exceptions of debt from discharge § 1:140 Tax claims § 1:141 Objections to discharge § 1:142 Objection to discharge proceedings § 1:143 Revocation of discharge § 1:144 Waiver of discharge § 1:145 Substantive consolidation XIV. SOURCES OF INFORMATION § 1:146 In general § 1:147 Notices to creditors § 1:148 The § 341 meeting of creditors § 1:149 Schedules and statements filed with the court § 1:150 Rule 2004 examinations CHAPTER 2. TAX COLLECTION OUTSIDE OF BANKRUPTCY I. ASSESSMENT AND DEFICIENCY PROCEDURES GENERALLY § 2:1 Assessment Authority § 2:2 Method of Assessment § 2:3 Notice and Demand for Tax § 2:4 Notice of Deficiency § 2:5 Petition to Tax Court after Notice of Deficiency § 2:6 Civil Actions for Refund II. LIEN FOR TAXES—GENERALLY § 2:7 Creation of Lien in Favor of United States § 2:8 Filing of Tax Lien by United States § 2:9 Period of Lien § 2:10 Invalidity of Unrecorded Federal Tax Lien Against Certain Persons § 2:11 —Against Purchaser § 2:12 —Against the Holder of a Security Interest § 2:13 —Against a Mechanic’s Lienor § 2:14 —Against a Judgment Lien Creditor III. RECORDED FEDERAL TAX LIENS (NOT IN BANKRUPTCY) § 2:15 Filing of Notice of Federal Tax Lien § 2:16 Protection for Certain Interests Against Recorded Federal Tax Lien § 2:17 —Purchaser of Securities § 2:18 —Purchaser of Motor Vehicles § 2:19 —Personal Property Purchased at Retail § 2:20 —Personal Property Purchased in Casual Sale § 2:21 —Personal Property Subject to Possessory Liens § 2:22 —Real Property Tax and Special Assessment Liens § 2:23 —Mechanic’s Lien for Residential Repairs § 2:24 —Attorneys’ Liens § 2:25 —Certain Insurance Contracts § 2:26 —Passbook Loans § 2:27 —Purchase Money Security Interest § 2:28 —Certain Commercial Transactions § 2:29 —Commercial Transactions Financing Agreements § 2:30 —Examples of Protection for Commercial Transactions Financing Agreements § 2:31 —Real Property Construction or Improvement Financing Agreement § 2:32 —Obligatory Disbursement Agreement § 2:33 —Certain Security Interests § 2:34 Priority of Interest and Expenses Over Unrecorded and Recorded Federal Tax Liens IV. SPECIAL RULES RELATING TO UNRECORDED AND RECORDED FEDERAL TAX LIENS § 2:35 Actual Notice or Knowledge § 2:36 Subrogation § 2:37 Disclosure of Amount of Outstanding Federal Tax Lien § 2:38 Special Liens for Estate and Gift Tax § 2:39 Proposed regulations on release of IRS liens CHAPTER 3. BANKRUPTCY COURT JURISDICTION OVER TAX MATTERS I. JURISDICTION OF THE BANKRUPTCY COURTS § 3:1 Congressional Authority Over Bankruptcy Matters § 3:2 The Bankruptcy Courts: A History § 3:3 Jurisdictional Aspects of the Bankruptcy Code Prior to Marathon § 3:4 Marathon § 3:5 The Aftermath of Marathon II. THE BANKRUPTCY AMENDMENTS AND FEDERAL JUDGESHIP ACT OF 1984 § 3:6 Legislative Responses to Marathon: The Bankruptcy Amendments and Federal Judgeship Act of 1984 § 3:7 Subject Matter Jurisdiction: 28 USC § 1334 § 3:8 —Referral to Bankruptcy Courts § 3:9 Core/Non-Core Distinction III. JURISDICTION OF BANKRUPTCY COURTS TO DETERMINE TAX LIABILITY § 3:10 Jurisdiction to Determine Tax Liability Pursuant to the Bankruptcy Act of 1898 § 3:11 Concurrent Jurisdiction of Bankruptcy and Other Courts to Determine Tax Liability Under the Bankruptcy Act of 1898 § 3:12 Legislative Precursors to § 505 of the Bankruptcy Code IV. AN OVERVIEW OF 11 USC § 505 § 3:13 Compromise by the House and Senate § 3:14 —Authority of Bankruptcy Courts to Rule on Merits of Tax Claims § 3:15 —Jurisdiction of Tax Court in Bankruptcy Cases § 3:16 —Audit of Trustee’s Returns § 3:17 —Immediate Assessment After Decision § 3:18 —Trustee’s Authority to Appeal Tax Cases V. DETERMINATION OF TAX MATTERS UNDER THE BANKRUPTCY CODE § 3:19 Power of the Court to Determine Tax Liability § 3:20 —Stage One: Determination of Prepetition Taxes § 3:21 —Stage Two: Determination of the Tax Liability of the Estate for the Period of Administration § 3:22 —Stage Three: Determination of Postconfirmation Tax Liability § 3:23 —State and Local Tax Issues § 3:24 —Federal Tax Issues § 3:25 Limitations on the Power of the Bankruptcy Court to Determine Tax Matters § 3:26 —Statutory Limits § 3:27 —Court Limits § 3:28 Permissive Abstention § 3:29 Immediate Assessment of Tax Following the Bankruptcy Court’s Determination of Liability § 3:30 Jurisdiction of Tax Court in Bankruptcy Cases § 3:31 Jurisdiction to Determine the Dischargeability of Tax Claims Against the Debtor § 3:32 Cases Interpreting § 505 § 3:33 Jurisdictional Provisions of Bankruptcy Reform Act of 1994 CHAPTER 4. SOVEREIGN IMMUNITY § 4:1 Waiver of Sovereign Immunity: § 106 § 4:2 Waiver Under § 106(a) § 4:3 Avoidance Actions § 4:4 —Stay and Discharge Violations § 4:5 —Must the IRS File A Claim, to Waive Sovereign Immunity? § 4:6 Waiver Under § 106(b) § 4:7 Waiver Under § 106(c) § 4:8 New § 106: Bankruptcy Reform Act of 1994 § 4:9 Waiver Under IRC § 7430 § 4:10 Waiver Under the Equal Access to Justice Act: 28 USC § 2412 CHAPTER 5. THE AUTOMATIC STAY I. ASSESSMENT AND DEFICIENCY PROCEDURES: AN OVERVIEW § 5:1 Assessment Authority § 5:2 Method of Assessment § 5:3 Notice and Demand for Tax § 5:4 Notice of Deficiency § 5:5 Petition to Tax Court after Notice of Deficiency § 5:6 Civil Actions for Refund II. DETERMINATION OF TAX LIABILITY UNDER THE BANKRUPTCY CODE § 5:7 Jurisdiction Under § 505(a)(1) of the Bankruptcy Code: An Overview § 5:8 Limitation of Jurisdiction under § 505 of the Bankruptcy Code III. THE AUTOMATIC STAY: § 362 § 5:9 Automatic Stay § 5:10 Scope of Automatic Stay § 5:11 —Stay of Proceedings: § 362(a)(1) § 5:12 —Control Over Property of the Estate: § 362(a)(3) § 5:13 —Liens: § 362(a)(4) § 5:14 —Tax Collection Efforts: § 362(a)(6) § 5:15 —Setoff and Freeze: § 362(a)(7) § 5:16 —Tax Court Proceedings: § 362(a)(8) § 5:17 Effect of Violating Stay § 5:18 Limits and Exceptions to Stay § 5:19 Cessation of Stay § 5:20 Relief from Automatic Stay § 5:21 Power to Enjoin the IRS § 5:22 Assets Seized By IRS Prior to Bankruptcy Filing § 5:23 Sanctioning the IRS for Willful Stay Violations IV. EFFECT OF STAY ON LIMITATIONS PERIODS § 5:24 Suspension of Statute of Limitations for Assessment or Collection of Taxes § 5:25 Suspension of Statute of Limitations for Filing Petition in Tax Court § 5:26 Trustee of Debtor’s Estate May Intervene in Tax Court Proceeding § 5:27 Period of Limitations on Civil Actions for Refund § 5:28 Right of Immediate Assessment CHAPTER 6. PROPERTY OF THE BANKRUPTCY ESTATE I. GENERALLY § 6:1 Introduction § 6:2 Property of the Estate: General Definition § 6:3 The Supreme Court’s Opinion in Whiting Pools § 6:4 —The Ownership Issue § 6:5 —The Importance of Whiting Pools § 6:6 Trust Fund Taxes Excluded from Property of the Debtor’s Estate § 6:7 The Supreme Court’s Opinion in Patterson v. Shumate § 6:8 The Estate in a Chapter 11 Case § 6:9 The Estate in a Chapter 13 Case II. TAX ATTRIBUTES § 6:10 Tax Attributes in an Individual’s Chapter 7 or 11 Case as Property of the Estate § 6:10.50 Avoidance Powers and Tax Attributes III. EXEMPTIONS § 6:11 Exempt Property in Bankruptcy § 6:12 Bankruptcy Exemptions § 6:13 Exemption Procedures § 6:14 Objections to Claims of Exemption § 6:15 The Exemption Avoidance Power IV. REDEMPTION § 6:16 The Debtor’s Right to Redeem Tangible Personal Property CHAPTER 7. THE CLAIMS PROCESS § 7:1 Claims, Generally § 7:2 Content of Claims and IRS Form 6338 § 7:3 Estimating Claims Under Bankruptcy Code § 502(c) § 7:4 Deadlines for Filing Claims § 7:5 —Chapter 7 Case § 7:6 —Chapter 11 Case § 7:7 —Chapter 13 Case § 7:8 Claims and Distribution § 7:9 Secured Claims § 7:10 Unsecured Claims § 7:11 Priorities Under the Bankruptcy Code § 7:12 Distribution to Creditors in a Chapter 11 Case § 7:14 Subordination Of Claims § 7:15 Bankruptcy from a Creditor’s Perspective § 7:16 Sources of Information Concerning the Debtor § 7:17 —Notices to Creditors § 7:18 —The § 341 Meeting of Creditors § 7:19 —Schedules and Statements Filed With the Court § 7:20 —Rule 2004 Examination § 7:21 Can a Debtor File a Proof of Claim on Behalf of the IRS? § 7:22 Informal Proof of Claim § 7:23 Reasons for the IRS Not to File a Claim § 7:24 Amendments to Proof of Claim Filed by the IRS § 7:25 Burden of Proof in Tax Contests CHAPTER 8. PRIORITIES OF UNSECURED TAX CLAIMS IN BANKRUPTCY I. INTRODUCTION § 8:1 Creation and Period of Unfiled Federal Tax Lien § 8:2 Invalidity of Unrecorded Federal Tax Lien Against Certain Persons § 8:3 —Against Purchaser § 8:4 —Against the Holder of a Security Interest § 8:5 —Against a Mechanic’s Lienor § 8:6 —Against a Judgment Lien Creditor II. PRIORITIES OF UNSECURED TAX CLAIMS IN BANKRUPTCY § 8:7 Applicability of Bankruptcy Code Chapters 1, 3, and 5 § 8:8 Waiver of Sovereign Immunity § 8:9 Tax Claims Given First Priority as Administrative Expenses § 8:10 Tax Claims Given Second Priority as Involuntary Gap Claims § 8:11 Certain Employment Taxes on Prepetition Wages Given Third Priority III. EIGHTH PRIORITY UNSECURED TAX CLAIMS § 8:12 Certain Income and Gross Receipts Taxes Given Eighth Priority § 8:13 Three-Year Rule § 8:14 240-Day Assessment Rule § 8:15 Still Assessable Rule § 8:16 Pro Rata Treatment § 8:17 Recent Property Taxes Given Eighth Priority § 8:18 Trust Fund Taxes Given Eighth Priority § 8:19 Employment Taxes Given Eighth Priority § 8:20 Excise Taxes Given Eighth Priority § 8:21 Customs Duty Given Eighth Priority § 8:22 Priority of Tax Penalty § 8:23 Priority for Erroneous Tax Refund or Credit § 8:24 Subrogation of Priority Claims IV. PRIORITIES AND DISTRIBUTIONS § 8:25 Priorities of Tax Claims Under The Bankruptcy Code § 8:26 Secured Claims § 8:27 Unsecured Claims § 8:28 Priorities Under Chapter 7 § 8:29 Distribution to Creditors in a Chapter 11 Case § 8:30 Interest on Deferred Tax Payments in Chapter 11 § 8:31 Distribution to Creditors in a Chapter 13 Case § 8:32 Subordination of Claims § 8:33 Treatment of Unsecured Priority Claims in Failed Chapter 11 Cases and Plans V. CHAPTER 11 CASES AND PLANS § 8:34 Treatment of Unsecured Tax Claims in Serial Chapter 11 Proceedings CHAPTER 9. FEDERAL TAX LIENS IN BANKRUPTCY I. FEDERAL TAX LIENS OUTSIDE OF BANKRUPTCY § 9:1 Filing of Notice of Federal Tax Lien § 9:2 Protection for Certain Interests Against Recorded Federal Tax Lien § 9:3 —Purchaser of Securities § 9:4 —Purchaser of Motor Vehicles § 9:5 —Personal Property Purchased at Retail § 9:6 —Personal Property Purchased in Casual Sale § 9:7 —Real Property Tax and Special Assessment Liens § 9:8 —Mechanic’s Lien for Residential Repairs § 9:9 —Attorney’s Liens § 9:10 —Certain Insurance Contracts § 9:11 —Passbook Loans § 9:12 —Purchase Money Security Interest § 9:13 —Certain Commercial Transactions § 9:14 —Commercial Transactions Financing Agreements § 9:15 —Examples of Protection for Commercial Transactions Financing Agreements II. FINANCING AGREEMENTS § 9:16 Real Property Construction or Improvement Financing Agreement § 9:17 —Obligatory Disbursement Agreement § 9:18 —Certain Security Interests § 9:19 Priority of Interest and Expenses Over Unrecorded and Recorded Federal Tax Liens III. SPECIAL RULES RELATING TO FEDERAL TAX LIENS § 9:20 Actual Notice or Knowledge § 9:21 Subrogation § 9:22 Disclosure of Amount of Outstanding Federal Tax Lien § 9:23 Special Liens for Estate and Gift Tax IV. PROPERTY TO WHICH FEDERAL TAX LIEN ATTACHES § 9:24 Lien Against Property of Taxpayer § 9:25 Property Exempt from Federal Tax Lien Levy V. FEDERAL TAX LIENS IN BANKRUPTCY § 9:26 Overview of Federal Tax Liens in Bankruptcy § 9:27 —Bifurcation Under Bankruptcy Code § 506(a) and the Extent of a Secured Claim § 9:28 —Surcharge Under Bankruptcy Code § 506(c) § 9:29 —Exemptions and the Federal Tax Lien § 9:30 —Postpetition After-Acquired Property VI. POWERS OF TRUSTEE AGAINST COLLATERAL CONSTITUTING PROPERTY OF THE ESTATE § 9:31 The Power to Use Collateral § 9:32 —The Power to Sell or Lease Collateral § 9:33 —The Power to Abandon Property § 9:34 —Agree to Stay Relief § 9:35 —Surrender of Collateral VII. A SECURED CREDITOR’S RIGHTS IN COLLATERAL § 9:36 The Right to Adequate Protection VIII. CASH COLLATERAL § 9:37 The Cash Collateral Contest IX. SPECIFIC TREATMENT OF FEDERAL TAX LIENS AND PRIORITY TAX CLAIMS IN BANKRUPTCY § 9:38 Federal Tax Liens in Chapter 7 § 9:39 —Partial Subordination of the Tax Lien in Chapter 7 § 9:40 Priority of Federal Tax Liens in Chapter 11 § 9:41 —Interest on Deferred Tax Payments Pursuant to Chapter 11 Plan § 9:42 Priority of Federal Tax Liens in Chapter 13 X. LIEN-STRIPPING § 9:43 Overview of Lien-Stripping § 9:44 —What is Lien-Stripping? § 9:45 Lien-Stripping in Chapter 7 § 9:46 Lien-Stripping in Chapter 13 § 9:47 Lien-Stripping in Chapter 11 § 9:47.50 Lien-Stripping in Chapter 12 § 9:48 Creditor Strategies in Response to Lien-Stripping § 9:49 Summary of Lien-Stripping in Chapters 13 and 11 CHAPTER 10. THE BANKRUPTCY DISCHARGE I. INTRODUCTION § 10:1 The Right to Discharge § 10:2 The Effect of the Bankruptcy Discharge § 10:3 The Chapter 7 Discharge § 10:4 Objections to Discharge § 10:5 The Chapter 11 Discharge § 10:6 The Chapter 13 Discharge § 10:7 The Discharge Hearing II. EXCEPTIONS OF CERTAIN DEBTS FROM DISCHARGE § 10:8 Exceptions From Discharge: Introduction § 10:9 Taxes Excepted from Discharge § 10:10 Taxes Excepted from Discharge in Chapter 11 Case § 10:11 Binding Effect of Chapter 11 Plan § 10:12 Federal Taxes Excepted from Discharge in Chapter 13 Case § 10:13 —Debts Provided for in the Chapter 13 Plan § 10:14 —Debts Disallowed Under Bankruptcy Code § 502 § 10:15 —Good Faith Confirmation Requirement; § 1325(a)(3) § 10:16 “Putting It All Together” in the Dischargeability Context § 10:17 Subrogation of Nondischargeable Claims § 10:18 Reduction of Nondischargeable Trust Fund Taxes § 10:19 —“Putting It All Together” in Trust Fund Taxes Scenario CHAPTER 11. THE TREATMENT OF TAX CLAIMS AND LIENS IN CHAPTER 7 § 11:1 Introduction § 11:2 Deadline by Which to File Proof of Claim § 11:3 Priorities Under Chapter 7 § 11:4 Priorities of Unsecured Tax Claims in Chapter 7 § 11:5 Federal Tax Liens in Chapter 7 § 11:6 Partial Subordination of the Tax Lien in Chapter 7 § 11:7 Lien-Stripping in Chapter 7 § 11:8 The Chapter 7 Discharge § 11:9 Taxes Excepted from Discharge § 11:10 The Separate Entity Rules: IRC § 1398 CHAPTER 12. TAX CLAIMS AND LIENS IN CHAPTER 11 § 12:1 Introduction § 12:2 Filing a Plan of Reorganization § 12:3 Contents of a Plan and Disclosure Statement § 12:4 Classification of Claims § 12:5 Funding Alternatives for Plan of Reorganization § 12:6 —Sale of Assets § 12:7 —Avoidance Powers § 12:8 —Postpetition Financing § 12:9 —Equity for Debt Swaps § 12:10 —Equity Infusions § 12:11 —Future Operations § 12:12 Acceptance and Confirmation of a Plan of Reorganization § 12:13 Plan Confirmation § 12:14 —Confirmation Under § 1129(a) of the Code § 12:15 —Cram Down § 12:16 Competing Plans § 12:17 Effect of Confirmation § 12:18 Modification of the Plan § 12:19 Priority of Unsecured Federal Tax Claims in Chapter 11 Reorganization Cases § 12:20 Interest on Deferred Tax Payments in Chapter 11 Reorganization Cases § 12:21 Postpetition Taxes, Penalties, and Interest in Chapter 11 Reorganization Cases § 12:22 Binding Effect on Tax Claims on Confirmation of the Reorganization Plan § 12:23 Priority of Secured Federal Tax Claims in Chapter 11 Reorganization Cases § 12:24 Postpetition Interest on Nonconsensual Secured Tax Claims § 12:25 Federal Taxes Excepted from Discharge in Chapter 11 Cases § 12:26 The Treatment of Tax Claims in Serial Chapter 11 Proceedings § 12:27 New professionals § 12:28 Ancillary and foreign proceedings CHAPTER 13. TAX CLAIMS AND LIENS IN CHAPTER 11—INDIVIDUAL DEBTOR CASES § 13:1 Introduction § 13:2 The Individual Debtor’s Chapter 11 Discharge § 13:3 Property of an Individual Debtor’s Bankruptcy Estate § 13:4 —The General Definition: § 541 § 13:5 —Future Earnings as Property of The Estate in a Chapter 11 Individual Debtor Case § 13:6 —Tax Attributes as Property of the Estate § 13:7 Separate Entity Rules: IRC § 1398 § 13:8 —The Mechanics of Taxing the Estate § 13:9 —The Determination of Income of the Estate § 13:10 —The Short-Year Election § 13:11 —The Consequences of the Election § 13:12 —Termination of the Estate CHAPTER 14. TAX CLAIMS AND LIENS IN CHAPTER 12 § 14:1 Introduction § 14:2 Eligibility Under Chapter 12 § 14:3 Role of the Chapter 12 Trustee § 14:4 Elements of the Chapter 12 Plan § 14:5 Confirmation of the Chapter 12 Plan § 14:6 Modification of the Chapter 12 Plan § 14:7 Effect of Confirmation § 14:8 Discharge Under Chapter 12 § 14:9 Priority of Unsecured Tax Claims in Chapter 12 § 14:10 Priority of Secured Tax Claims in Chapter 12 § 14:11 Tax Excepted from Discharge in Chapter 12 § 14:12 Setoff of Income Tax Refunds § 14:13 Internal Revenue Service Alternatives for Collecting Postconfirmation Tax Claims in Chapter 12 § 14:14 Conversion or Dismissal of a Chapter 12 Case § 14:15 Overview of lien-stripping § 14:16 What is lien-stripping? § 14:17 Lien-stripping in Dewsnup v. Timm § 14:18 Lien-stripping in Chapter 12 CHAPTER 15. TAX CLAIMS AND LIENS IN CHAPTER 13 § 15:1 Eligibility Under Chapter 13 § 15:2 Role of the Chapter 13 Trustee § 15:3 Elements of the Plan § 15:4 Confirmation of the Plan § 15:5 Modification of the Plan § 15:6 Effect of Confirmation § 15:7 Discharge Under Chapter 13 § 15:8 Priority of Unsecured Tax Claims in Chapter 13 § 15:9 Priority of Secured Tax Claims in Chapter 13 § 15:10 Taxes Excepted from Discharge in Chapter 13 § 15:11 Setoff of Income Tax Refunds § 15:12 Priority and Collection of Postpetition Tax Claims Under 1305 § 15:13 Internal Revenue Service Alternatives for Collecting Postconfirmation Tax Claims in Chapter 13 § 15:14 Conversion or Dismissal of a Chapter 13 Case § 15:15 Overview of Lien-Stripping § 15:16 —What is Lien-Stripping? § 15:17 Lien-Stripping in Dewsnup v. Timm § 15:18 Lien-Stripping in Chapter 13 CHAPTER 16. AVOIDABLE PREFERENCES I. INTRODUCTION § 16:1 Purpose of the Avoidance Powers § 16:2 General Considerations—Proper Plaintiff § 16:3 —Limitation On Time for Commencing Preference Action § 16:4 —Procedural Considerations II. ELEMENTS OF AN AVOIDABLE PREFERENCE ACTION § 16:5 Elements of a Preference § 16:6 Burden of Proof § 16:7 Transfer § 16:8 Debtor’s Interest in Property § 16:9 To or for the Benefit of a Creditor § 16:10 For or on Account of an Antecedent Debt § 16:11 The Debtor is Insolvent § 16:12 Made on or Within 90 Days § 16:13 Preferential Effect § 16:13.50 Fraudulent transfer provisions III. AFFIRMATIVE DEFENSES § 16:14 Contemporaneous Exchanges § 16:15 Payment Made in the Ordinary Course of Business § 16:15.50 Avoidance of statutory tax liens prohibited—§ 545(2) § 16:16 Enabling Loans § 16:17 Subsequent Advancement of Unsecured Credit § 16:18 Floating Liens § 16:19 Support and Alimony § 16:20 Certain Consumer Debts § 16:21 Effect of Federal Tax Lien § 16:22 Sovereign Immunity CHAPTER 17. THE INNOCENT SPOUSE DEFENSE IN BANKRUPTCY I. JOINT TAX RETURNS § 17:1 Joint Tax Returns II. INNOCENT SPOUSE DEFENSE OUTSIDE OF BANKRUPTCY § 17:2 The Innocent Spouse Act of 1971 (As Amended) § 17:3 The 1984 Version of the Innocent Spouse Defense Under 6013(e) § 17:4 No Basis in Fact or Law Under § 6013(e) § 17:5 Reason to Know Under § 6013(e) § 17:6 Summary of Defenses Outside of Bankruptcy Under 6013(e) § 17:7 New § 6015—Overview § 17:8 New § 6015(b)—Requirements for Relief § 17:9 New § 6015(c)—Divorced and Separated Taxpayers § 17:10 New § 6015(d) – Allocation of Deficiency for Purposes of 6015(c) § 17:11 New § 6015 (e)—Review by Tax Court § 17:12 New §§ 6015(f) and (g)—Equitable Relief, Credits and Refunds III. INNOCENT SPOUSE DEFENSE IN BANKRUPTCY § 17:13 Jurisdiction to Determine Defense Under § 6013(e) § 17:14 Bankruptcy Cases Interpreting the Defense Under 6013(e) § 17:15 Appellate Cases Interpreting the Defense Under § 6015 § 17:16 Bankruptcy Cases Interpreting the Defense Under § 6015 CHAPTER 18. COMPROMISE AND SETTLEMENT OF TAX LIABILITIES § 18:1 Introduction to Offer in Compromise § 18:2 What Are the Reasons for the IRS to Compromise a Tax Liability? § 18:3 What Is IRS Policy Statement P-5-100? § 18:4 How Do You Prepare an Acceptable Offer in Compromise to Submit to the IRS? § 18:5 Will the IRS Conduct an Independent Investigation Concerning Any Offer in Compromise? § 18:6 What Questions Will the IRS Consider When Reviewing the Taxpayer’s Offer of Compromise? § 18:7 Are There Any Other Additional Requirements the IRS May Impose Concerning the Offer in Compromise? § 18:8 Are There Any Tax Compliance Issues That Must Be Addressed By the Taxpayer? § 18:9 Is the IRS Required to Suspend Any Collection Activity on Submission of an Offer in Compromise By the Taxpayer? § 18:10 What Are the Consequences to the Taxpayer on Submitting an Offer in Compromise? § 18:11 Where Should the Offer in Compromise Be Filed? § 18:12 What Remedies Are Available to the Taxpayer in the Event the IRS Rejects the Taxpayer’s Offer in Compromise? § 18:13 Will the Taxpayer’s Offer in Compromise Become a Public Record? § 18:14 Is an Offer in Compromise With the IRS a Viable Alternative to Bankruptcy? § 18:15 Offers in Compromise in Bankruptcy CHAPTER 19. DEBTOR’S AND TRUSTEE’S REPORTING AND COMPLIANCE ISSUES I. INTRODUCTION § 19:1 Pre-1980 Law § 19:2 Bankruptcy Tax Act of 1980 II. ACCOUNTING PERIODS OF DIFFERENT ENTITIES § 19:3 Individuals § 19:4 Corporations § 19:5 Partnerships and Other Entities III. INCOME TAX RETURNS § 19:5.50 Bankruptcy Code tax filing requirements § 19:6 Individuals § 19:7 Corporations § 19:8 Partnerships § 19:9 Other Entities IV. PAYROLL TAXES § 19:10 Trustee’s Duty to Withhold § 19:11 Withholding Employment Taxes for Wages Earned Prior to Bankruptcy § 19:12 Reports and Returns § 19:13 Withholding Employment Taxes on Trustee’s Commissions V. PENALTIES AND INTEREST § 19:14 Employment and Withholding Tax Penalties § 19:15 Civil Penalties § 19:16 Interest VI. PROCEDURAL POINTERS FOR THE DEBTOR AND THE TRUSTEE § 19:17 Relief from Certain Failures to Pay Tax When Due § 19:18 Preservation of Credit for Federal Unemployment Tax (FUTA) § 19:19 IRS provides favorable ruling on aging of individual taxes in disaster areas and combat zones CHAPTER 20. THE SEPARATE ENTITY RULES: IRC 1398 § 20:1 Introduction § 20:2 Prior Law § 20:3 When Does IRC § 1398 Apply? § 20:4 May a Partnership Take Advantage of IRC § 1398? § 20:5 What Is the Purpose of IRC § 1398? § 20:6 How Is the Bankruptcy Estate Taxed Pursuant to IRC 1398? § 20:7 Does IRC § 1398(c)(1) Make a Trustee Personally Liable for Estate Taxes if There is a Deficiency After the Estate Assets Are Distributed? § 20:8 Must a Trustee File a Federal Tax Return Where the Estate Has Generated No Income Through Operations? § 20:9 How Is the Gross Income of a Bankruptcy Estate Determined? § 20:10 How Is Income Treated Where a Debtor Earned the Income Prior to the Date the Petition Was Filed, But the Income Was Received By the Bankruptcy Estate? § 20:11 How Is Cancellation of Indebtedness Income Treated Under the Separate Entity Rules? § 20:12 How Are Deductions Treated Under the Separate Entity Rules? § 20:13 Are Transfers of Assets Between the Debtor and the Estate Taxable Events? § 20:14 Does the Estate Succeed to the Debtor’s Tax Attributes? § 20:15 Is IRC § 1398(g) Redundant and Unnecessary? § 20:16 What Is a “Short-Year” Election? § 20:17 Short-Year Election By Individual Debtor § 20:18 Short-Year Election By Married Debtor § 20:19 When Must the Short-Year Election Be Made By a Debtor? § 20:20 What Is the Effect of Making the Short-Year Election? § 20:21 Can a Debtor or Nondebtor Spouse Join in the Election? § 20:22 When Is It Advisable for a Debtor to Make the Short-Year Election? § 20:23 Termination of the Estate § 20:24 Proposed Change to Default Rule Regarding Election § 20:25 Partners, Partnerships, and the Separate Entity Rules § 20:26 Prior Law Relating to Partners and Partnerships § 20:27 Present Law Relating to Partners and Partnerships § 20:28 —Partner’s Basis in Partnership § 20:29 Treatment of Partnership Debt—Bankrupt or Insolvent Partner § 20:30 —Solvent Partner § 20:31 Depreciable Property—Recapture Rules § 20:32 Conclusion CHAPTER 21. STATE AND LOCAL TAXES § 21:1 Introduction § 21:2 Is a New Taxable Entity Created for State and Local Income Tax Purposes When an Individual Debtor Files a Bankruptcy Petition Under Chapter 7, 11, or 12? § 21:3 Is a New Taxable Entity Created for State and Local Income Tax Purposes When a Corporation or Partnership Files a Bankruptcy Petition Under Chapter 7, 11, or 12? § 21:4 Is a New Taxable Entity Created for State and Local Income Tax Purposes When an Individual Debtor Files a Chapter 13? § 21:5 Who Is Responsible for Filing the State and Local Income Tax Returns for the Bankruptcy Estate of an Individual Debtor, a Corporate Debtor, or a Partnership Debtor? § 21:6 What Is the Taxable Period or Year for State and Local Income Tax Purposes When an Individual Debtor Files a Bankruptcy Petition Under Chapter 7, 11, or 12? § 21:7 Are There Any Tax Consequences for State and Local Income Tax Purposes When Property Is Transferred From the Individual Debtor to the Bankruptcy Estate Under Chapter 7, 11, or 12? § 21:8 Does the Bankruptcy Estate Succeed to an Individual Debtor’s Tax Attribute for State and Local Income Tax Purposes Under Chapter 7, 11, or 12? § 21:9 What Are the Special Rules Dealing With Net Operating Loss (NOL) or Other Carrybacks of an Individual Debtor for State and Local Income Tax Purposes Under Chapter 7, 11, or 12? § 21:10 What is the General Rule About Forgiveness or Cancellation of Indebtedness for State and Local Income Tax Purposes? § 21:11 Can Liabilities Which Are Deductible and Which Are Also Canceled or Forgiven Be Deducted for State and Local Income Tax Purposes? § 21:12 Is the Debtor Required to Reduce Any Tax Attributes for State and Local Income Tax Purposes When the Debtor Realizes Cancellation of Indebtedness (COD) Income? § 21:13 What Are the Exceptions to the Rule that Net Operating Losses (NOL’s) Must Be Reduced for State and Local Income Tax Purposes When the Debtor Realizes Cancellation of Indebtedness (COD) Income? § 21:14 What Is the Two-Point Test for the Reduction of Basis of the Debtor’s Property for State and Local Income Tax Purposes? § 21:15 Can the Debtor Elect Between Reducing the Basis of the Debtor’s Property or Treating Cancellation of Indebtedness (COD) Income as Taxable Income for State and Local Income Tax Purposes? § 21:16 Does Cancellation of Indebtedness (COD) Income Include for State and Local Income Tax Purposes, Debt Not of a Deductible Nature Exchanged for Stock Pursuant to a Plan of Reorganization? § 21:17 Does Cancellation of Indebtedness (COD) Income Include for State and Local Income Tax Purposes, Debt Not of a Deductible Nature, That Is Forgiven as a Contribution to Capital by an Equity Security Holder? § 21:18 Does Cancellation of Indebtedness (COD) Income Include for State and Local Income Tax Purposes, Debt of a Deductible Nature Exchanged for Stock When Such Exchange Has the Effect as a Cash Payment? TAX ASPECTS OF BANKRUPTCY LAW 3D xxviii § 21:19 What Priority is Given Under the Bankruptcy Code to a Prepetition Unsecured State and Local Tax Measured By Income or Gross Receipts? § 21:20 What Priority is Given Under the Bankruptcy Code to a Postpetition Unsecured, State and Local Tax Measured By Income or Gross Receipts? § 21:21 What Priority Is Given Under the Bankruptcy Code for State and Local Tax Purposes to Employment Taxes on Prepetition Wages? § 21:22 What Priority Is Given Under the Bankruptcy Code for State and Local Tax Purposes to Prepetition Unsecured Trust Fund Taxes? § 21:23 What Priority Is Given Under the Bankruptcy Code for State and Local Tax Purposes to a Prepetition Unsecured Employment Tax? § 21:24 What Priority Is Given Under the Bankruptcy Code for State and Local Tax Purposes to a Prepetition Unsecured Excise Tax? § 21:25 What Priority Is Given Under the Bankruptcy Code for State and Local Tax Purposes to a Prepetition Unsecured Property Tax? § 21:26 What Priority Is Given Under the Bankruptcy Code for State and Local Tax Purposes to a Prepetition Secured Claim for Property Taxes? § 21:27 Can a State or Local Government Impose a Stamp Tax or Similar Tax on the Transfer or Issuance of a Security Pursuant to a Confirmed Plan of Reorganization Under Chapter 11 or 12? § 21:28 Can the Bankruptcy Court Authorize the Proponent of a Plan of Reorganization Under a Chapter 11 or 12 to Request a Ruling on a Tax Issue for State and Local Income Tax Purposes? § 21:29 What Is the Marshalling Rule Pertaining to State and Local Income Tax Claims Against a Partner and a Partnership in a Case Under Chapter 7? § 21:30 Is the Bankruptcy Court Required to Apportion for State and Local Income Tax Purposes Any Tax Refund or Reduction of Tax Between the Bankruptcy Estate of a Partner and the Bankruptcy Estate of His or Her Partnership Under Chapter 7? CHAPTER 22. CANCELLATION OF INDEBTEDNESS PRIOR TO 1980 ACT I. JUDICIALLY DEVELOPED RULES § 22:1 Judicially Developed Rules Generally § 22:2 Recognition of Income: The Kirby Lumber Rule § 22:3 Amount of Gain § 22:4 Time of Realization of Income § 22:5 Character of Income Recognized TABLE OF CONTENTS xxix § 22:6 Debt Cancellation by Gift § 22:7 Shareholder’s Cancellation of Corporate Debt § 22:8 —Extension of the Contribution to Capital Rule § 22:9 —Summary § 22:10 Cancellation of a Partnership Debt § 22:11 Issuance of Stock or Bonds in Satisfaction of Corporate Debt § 22:12 The Tax Benefit Rule § 22:13 Assignment of Income Rule § 22:14 Cancellation of Purchase Money Obligations § 22:15 —The Crane Rule § 22:16 —Circuit Court Interpretation of Crane § 22:17 —Supreme Court Interpretation of Crane § 22:18 Compromise of Contingent or Disputed Obligations § 22:19 Debt Exchanged for Contingent Debt or Guarantees § 22:20 Renegotiated Purchase Price § 22:21 Cancellation as Reimbursement for Loss § 22:22 Net Loss on the Transaction § 22:23 No Increase in the Debtor’s Assets § 22:24 The Insolvency Exception § 22:25 —Further Development of the Insolvency Exception § 22:26 Summary of Exceptions II. PRIOR STATUTORY LAW GOVERNING FORGIVENESS OF DEBT § 22:27 Prior Statutory Law § 22:28 Election to Exclude Income § 22:29 Meaning of Income § 22:30 Basis Adjustments Generally § 22:31 Formal Consent Required § 22:32 Order of Adjustment to the Tax Basis of Assets § 22:33 Other Effects of the Election § 22:34 Earnings and Profits CHAPTER 23. CANCELLATION OF INDEBTEDNESS UNDER THE 1980 ACT I. INTRODUCTION § 23:1 Generally § 23:2 Prior Law § 23:3 New Law II. DEFINITIONS § 23:4 Generally § 23:5 Indebtedness of the Taxpayer § 23:6 Title 11 Case TAX ASPECTS OF BANKRUPTCY LAW 3D xxx § 23:7 Insolvent § 23:8 Depreciable Property III. DETERMINATION OF COD INCOME § 23:9 When Does a Taxpayer Not in Bankruptcy Recognize COD Income? § 23:10 How do You Determine the Amount of the COD Income? § 23:11 Must the Taxpayer File Any IRS Form in Order to Qualify for the Exclusion of COD Income from Gross Income? § 23:12 Information Return by Certain Financial Entities § 23:13 When Does a Taxpayer in Bankruptcy Realize COD Income? § 23:14 What Does IRC § 108 Require a Taxpayer in Bankruptcy or Insolvent Taxpayer to Do with COD Income? IV. EXCEPTIONS TO CANCELLATION OF INDEBTEDNESS RULE § 23:15 Purchase Money Debt § 23:16 Capital Contributions § 23:17 Stock for Debt—General Rule § 23:18 —De Minimis Cases § 23:19 —Other Property § 23:20 —Recapture Rule § 23:21 Section 108(a)(1)(D) Qualified Real Property Indebtedness V. IMPLICATIONS FOR PARTNERSHIP AND S CORPORATION DEBT § 23:22 Discharge of Partnership Debt § 23:23 Discharge of S Corporation Debt VI. MISCELLANEOUS PROVISIONS § 23:24 Related Parties § 23:25 Other Provisions within § 108—REITs, Reduction of Tax Attributes, Student Loans, and Farm Debt § 23:26 Other Provisions Related to § 108—Tax Benefit Rule and Earnings and Profits Rule VII. TRANSFER OF PROPERTY IN SATISFACTION OF DEBT § 23:27 In General § 23:28 General Rule: Two-Step Analysis § 23:29 Impact of § 108 Election § 23:30 Insolvency: One-Step Analysis § 23:31 Nonrecourse Mortgages: One-Step Analysis § 23:32 Impact of Bankruptcy Tax Act of 1980 TABLE OF CONTENTS xxxi CHAPTER 24. THE TAX CONSEQUENCES OF ABANDONMENT § 24:1 Introduction § 24:2 The Separate Entity Rules § 24:3 —Prior Law § 24:4 —Section 1398 of the Bankruptcy Tax Act of 1980 (BTA) § 24:5 The Power of Abandonment § 24:6 Abandonment Under the Bankruptcy Act § 24:7 Abandonment Under the Bankruptcy Code § 24:8 Limitations on the Abandonment Power § 24:9 Effect of Abandonment § 24:10 Developing a Comprehensive Abandonment Model § 24:11 The Abandonment Model of In re Olson § 24:12 The Abandonment Model of In re A.J. Lane & Co § 24:13 The Tax Attribute Abandonment Model § 24:14 The ABA Abandonment Model § 24:15 The National Bankruptcy Conference Abandonment Model § 24:16 A Proposed Coherent Abandonment Model § 24:17 Arguments for the Proposed Coherent Abandonment Model § 24:18 Deductibility of Home Mortgage Interest Upon Short-Sell, Abandonment, and Discharge CHAPTER 25. PRESERVING TAX ATTRIBUTES § 25:1 Historical Development § 25:2 Avoiding Income Recognition § 25:3 What Attributes Are Reduced By a Taxpayer in Bankruptcy? § 25:4 What Is the Amount Required for Attribute Reduction By a Taxpayer in Bankruptcy? § 25:5 What Is the Timing Required for Attribute Reduction By a Taxpayer in Bankruptcy? § 25:6 Who Is the Taxpayer in a Bankruptcy Case That Accounts for the Reduction of the Tax Attributes? § 25:7 Who Is an Insolvent Taxpayer Not in Bankruptcy? § 25:8 What Tax Attributes Must Be Reduced By an Insolvent Taxpayer Not in Bankruptcy? § 25:9 Examples of Attribute Reduction for a Taxpayer in Bankruptcy and an Insolvent Taxpayer Not in Bankruptcy § 25:10 What Is Depreciable Property? § 25:11 Election to First Reduce Basis in Depreciable Property— By Taxpayer in Bankruptcy and Insolvent Taxpayer Not in Bankruptcy § 25:12 Timing of Basis Reduction § 25:13 Examples of Basis Reduction § 25:14 Recapture Rules § 25:15 Consolidated attribute reduction TAX ASPECTS OF BANKRUPTCY LAW 3D xxxii CHAPTER 26. NONTAXABLE TRANSACTIONS I. BANKRUPTCY REORGANIZATIONS § 26:1 In General II. OVERVIEW OF PRIOR LAW § 26:2 Introduction § 26:3 Judicial Principles—Continuity of Interest § 26:4 —Continuity of Business Enterprise § 26:5 Statutory Law III. CHANGES UNDER THE BANKRUPTCY TAX ACT OF 1980 § 26:6 Section 368(a)(1)(G) Replaces § 371 § 26:7 General Requirements § 26:8 —Title 11 or Similar Case § 26:9 —Qualification under §§ 354, 355, or 356 § 26:10 —Other Rules § 26:11 Carryover of Tax Attributes: §§ 381 and 382 IV. OPERATIVE PROVISIONS § 26:12 Treatment of the Transferor § 26:13 Treatment of Shareholders and Creditors V. OTHER REORGANIZATIONS § 26:14 In General § 26:15 Alternative Reorganization VI. TAX-FREE TRANSFERS TO CONTROLLED CORPORATIONS § 26:16 Purpose of § 351 § 26:17 Prior Law § 26:18 New Law CHAPTER 27. PRESERVATION OF NET OPERATING LOSSES I. TAX ATTRIBUTES OF FINANCIALLY TROUBLED CORPORATIONS § 27:0.50 Net Operating Loss (“NOL”) Changes § 27:1 Introduction § 27:2 Pre-1954 Code Treatment II. ACQUISITIONS TO EVADE OR AVOID INCOME TAX—§ 269 § 27:3 In General TABLE OF CONTENTS xxxiii § 27:4 The Forbidden Purpose § 27:5 —Permitted Purpose § 27:6 Control § 27:7 Post-acquisition Losses III. DISALLOWANCE OF NET OPERATING LOSSES— § 382(A) § 27:8 In General § 27:9 Change in Ownership § 27:10 —Effect of Change in Ownership § 27:11 Change in Business § 27:12 —Temporary Suspension of Business § 27:13 —Change of Location § 27:14 —Discontinuing Part of Business § 27:15 —Liquidating a Subsidiary § 27:16 Post-1986 Change of Ownership § 27:17 Ownership Change § 27:18 Continuity of Business § 27:19 Bankrupt and Insolvent Corporations § 27:20 Built-In Gains Offset by Pre-acquisition Losses IV. LIQUIDATIONS § 27:21 In General § 27:22 Section 337 Liquidation § 27:23 Section 333 Liquidation § 27:24 Section 332 Liquidation § 27:25 Corporate Distributions CHAPTER 28. INTEREST, EXPENSES AND RECAPTURE I. INTEREST EXPENSE OF DEBTORS § 28:1 In General § 28:2 Impact of Financial Distress § 28:3 Related Parties § 28:4 Summary II. INTEREST INCOME OF ACCRUAL BASIS CREDITORS § 28:5 In General § 28:6 Impact Where Collection Unlikely § 28:7 Intercompany Loans III. DEDUCTIBILITY OF BANKRUPTCY EXPENSES § 28:8 Administration Expenses of an Individual Debtor TAX ASPECTS OF BANKRUPTCY LAW 3D xxxiv § 28:9 Expenses of Debtor Corporations and Partnerships IV. RECAPTURE OF INVESTMENT TAX CREDIT BY TAXPAYERS IN BANKRUPTCY § 28:10 Prior Law § 28:11 Impact of the Bankruptcy Tax Act of 1980 APPENDIX Appendix A. Tax Report Final Report of the Tax Advisory Committee to the National Bankruptcy Review Commission (August 1997, Washington, D.C.) Table of Laws and Rules Table of Cases Index TABLE OF CONTENTS xxxv

A lawyer is a person who writes a 10,000-word document and calls it a "brief."

Franz Kafka